By David Lucas

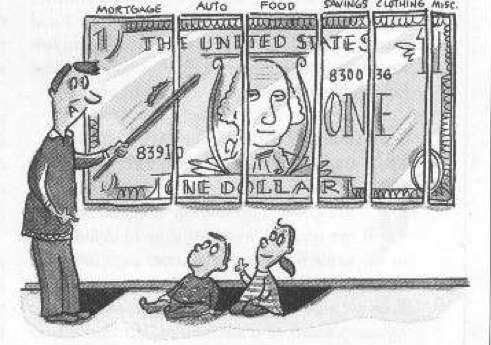

It is very important to teach your children wile they are young to be wise with their money. All of the basics we have learned when we were younger played a critical role in our lives and our education. We still use the things we learned in elementary school in our everyday lives. Why should financing be any different? If our children learn that they can purchase anything they want then that is what they will always expect. They will have a hard time knowing how to handle their money and how to use it in a smart way. To teach your children you must make sure that you are practicing your finance in a good way. What you do reflect upon them. Start off by introducing your children to money and tell them some of the things it is used for. Giving your children an allowance will give them a chance to actually handle money. They will get a feel of what it is like to receive money, use, and save. They will find out what it is like to have money and then just as easily not have it. This will give them a building block learning approach to how they want to handle and save their money. They might want a toy and they will know they need to set money aside to get it. As they get older you can teach them more about credit. If they need to borrow some money teach them that they will have to pay back. Teaching children how to use money when they are young because they will grow up knowing that positives and negatives that can come from having and using money.

http://www.thedigeratilife.com/blog/index.php/2009/01/30teach-children-about-money-lessons-kids-should-learn/

http://www.thepersonalfinacier.com/2008/07/teach-your-kids-basic-finance-and.html

{kind=link}